What does 2025 hold for AFS License Holders and its financial advisers.

As we welcome the new year, over the next few weeks, we would will explore and examine the challenges and regulatory changes that we expect the market to face in the next 12 months.

While we have seen significant regulatory changes occurring in the last few years, it appears that there is more on the horizon.

“We don't necessarily see a light at the end of the tunnel yet, so I would argue that it will be again, front and centre in 2025 for advisers,” ( Aaron Dunn, CEO of Smarter SMSF)

The DBFO Act

Background

Following 10 months of consultation, independent reviewer, Michelle Levy, handed the Quality of Advice Review (QAR) final report to government on 16 December 2022. The government responded to 14 of the 22 recommendations made in the QAR report.

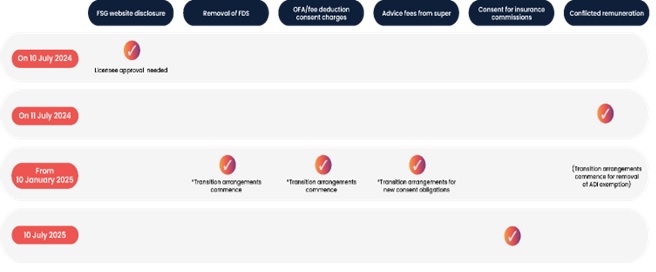

With a focus on improving access to financial advice, the ‘Delivering Better Financial Outcomes’ package of reforms implements the government’s final QAR roadmap in two tranches which are graphically represented below.

Transition arrangements and key dates

Website FSG Disclosure

The first transition arrangement occurred on 10 July 2024, where Schedule 1, Part 3 of the DBFO Act allowed for financial product advice providers to either continue providing an FSG or make the FSG information publicly available on their website.

The purpose of an FSG is to ensure that retail clients receive key information about the type of financial services being offered and the fees charged. At Novus, we elected to not adopt this change and continue to provide each retail client with an FSG.

Removal of Fee Disclosure Statements (FDs)

One of the most eagerly awaited changes of the DBO Act, is the removal of the Fee Disclosure Statements which is included in Schedule 1, Part 2 of the DBFO Act and confirms Treasury’s response to recommendation 9 of the QAR.

From 10 January 2025, new requirements relating to ongoing fee arrangements (OFAs) and product consents will apply.

The reform consolidates and streamlines the consent process when clients enter or renew ongoing fee arrangements and authorise ongoing fees to be deducted from a financial product. The obligation for fee recipients to give clients a fee disclosure statement annually is removed by the DBFO Act.

Transitional arrangements apply to the DBFO Act and FDS

- entered into or last renewed before 10 January 2025 (start day), and

- for ongoing fee arrangements in force on the start day, until the first anniversary of the arrangement that occurs on or after the start day.

While the goal of this legislation is to streamline these processes, practical challenges remain with the management of transitional clients.

Under the DBFO Act reforms, FDSs and the old OFA renewal requirements will be replaced with new consent requirements relating to entering into an OFA and paying fees. These reforms are not explicit in its understanding and will require advisers to closely review their existing arrangements and work with their AFSL to develop new documents and client notices.

ASIC has released Information Sheet 286 FAQs: Ongoing fee arrangements and consents and Information Sheet 287 FAQs: Non-ongoing fee requests or consents. It would be prudent to look at these when preparing processes for the new OFA regime.

WHY NOVUS CAPITAL?

WHY NOVUS CAPITAL?